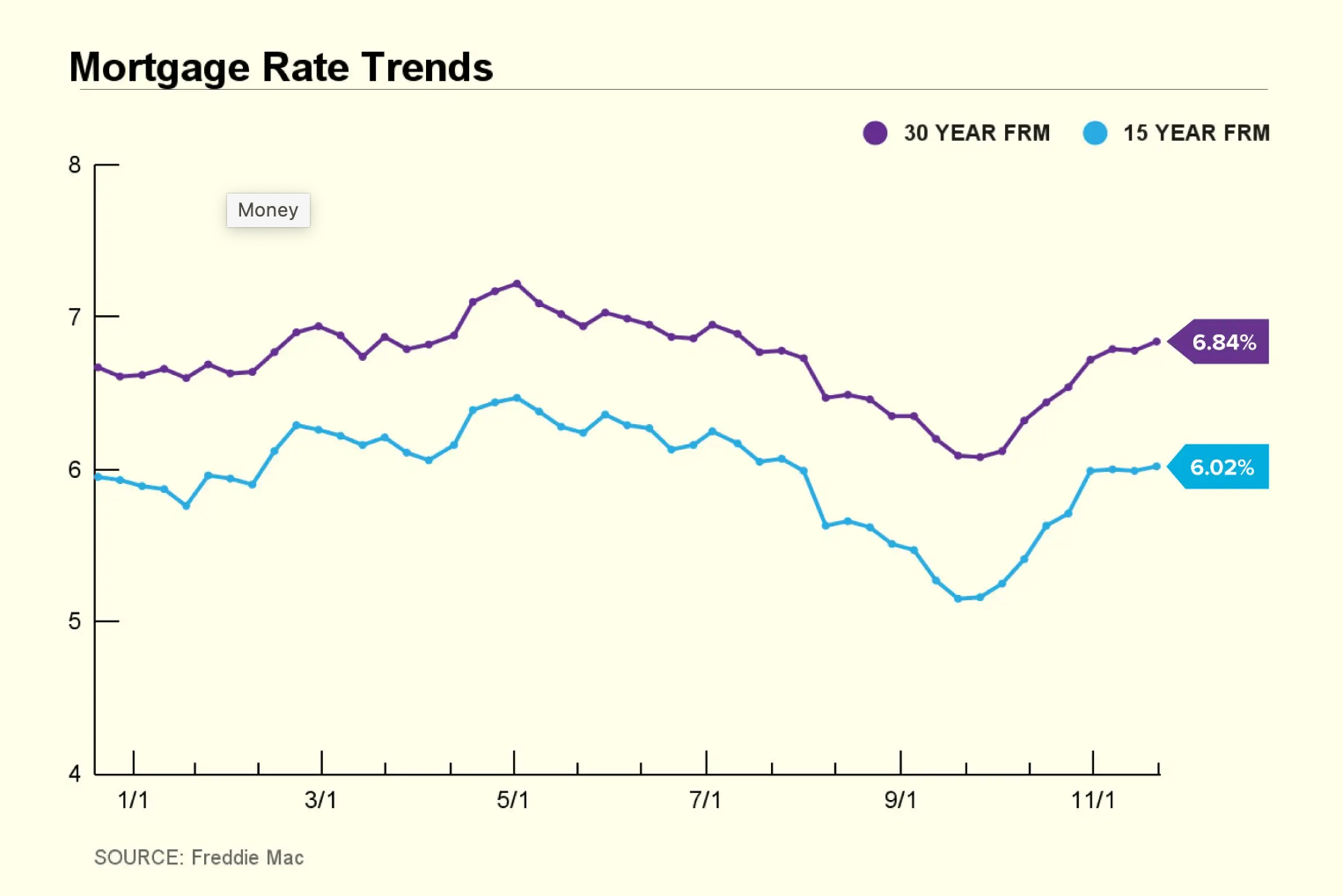

Expert Predictions for Mortgage Rates in 2025

Experts generally predict that mortgage rates will decrease steadily in 2025, although the reduction is expected to be gradual rather than dramatic. Both the Mortgage Bankers Association (MBA) and Fannie Mae support this outlook, with rates expected to start the year around 6.2% and potentially fall to 5.9% by the end of 2025. Fannie Mae forecasts an even more modest drop, from 5.9% to 5.6%. Experts suggest that rates will likely settle in the mid-5% range, which, while higher than pre-pandemic levels, would still be historically low and supportive of a healthy economy.

The path to these lower rates, however, is expected to be somewhat unpredictable, with slight fluctuations along the way. Mike Hardy from Churchill Mortgage likens the trend to a “kid on a down escalator with a yo-yo,” suggesting that while rates will generally trend downward, there will be occasional upswings.

While the outlook for lower rates is positive, experts caution that waiting too long to buy a home could backfire. As more buyers wait for rates to drop, the demand for housing will increase, potentially driving home prices higher in 2025. Hardy predicts home prices could rise by 4% to 5%, which could make homes more expensive than they are today. For those who can afford to buy now, experts recommend doing so and then refinancing in a year or two when rates are even more favorable.

In conclusion, mortgage rates are expected to trend down in 2025, but the reduction will likely be gradual. Buyers who wait for significantly lower rates may face higher home prices and more competition, making it a potentially better strategy to purchase a home sooner and refinance later.

The following are the forces that will influence mortgage rates over the coming year:

The best events, hikes and activities in Spring in Phoenix and Scottsdale

Real estate trends and statistics in Phoenix, Carefree, Cave Creek, Scottsdale, and surrounding areas.

Data and predictions for 2026

The time-tested crowd favorites to visit in December

Real estate news in the Phoenix metro area

Sereno Canyon in North Scottsdale

Navigating a Shift Towards Balance in October 2025

Bringing together a team with the passion, dedication, and resources to help our clients reach their buying and selling goals. With you every step of the way.

Get In Touch With Our Team To Learn More

Falkner | Cohen Group

6201 East Cave Creek Rd., Suite B Cave Creek, AZ, 85331